National Saving Certificate (NSC) is a Post Office Savings Scheme which also saves income tax as deposits qualify for deduction under section 80C of Income Tax Act. There is no maximum limit for investment in National Savings Certificates, minimum amount is Rs. 1000 and in multiple of Rs. 100. National Saving Certificate Interest Rate 2026 is fixed at 7.7% (from 1 October 2023) compounded p.a and to check it using National Saving Certificate Calculator. Moreover, people can firstly check NSC interest rate chart and fill NSC online application form to apply for this central government run India Post Office Scheme.

National Saving Certificate (NSC) Scheme of Post Office

NSC Interest Rate Chart shows that the nsc interest rate is at par with other schemes like Public Provident Fund (PPF), Kisan Vikas Patra (KVP), Sukanya Samriddhi Yojana, Post Office Savings Account, Recurring Deposit (RD) Account, Senior Citizen Saving Scheme (SCSS), Time Deposit (TD) Account, Monthly Income Scheme (MIS). People can now compare and check nsc vs ppf vs kvp vs ssy vs scss vs mis vs rd vs td vs post office savings account.

In this article, we will tell you about the NSC account maturity period, deposits, pledging of account, premature closure and transfer of account. National savings scheme rate of interest is low and is taxable only at the time of maturity. People can use national saving certificate as collaterals and can take loans from banks. NRI, HUF and Trusts are not eligible to invest and purchase National Saving Certificate (NSC). People can Compare All Post Office Schemes before making investment.

Types of National Savings Certificates in NSC Scheme

There are 3 types of National Saving Certificate which are as follows:-

- Single Holder Type Certificate - Any individual can purchase National Saving Certificate for himself or on the behalf of a minor.

- Joint A Type Certificate - This type of NSC is issued to 2 adults jointly which is payable to both the NSC account holders.

- Joint B Type Certificate - This NSC certificate type is issued jointly to 2 adults which is payable to either of the NSC account holders.

People can redeem National Saving Certificates only after the NSC maturity period on submission of certificate at post office. Moreover on receipt of maturity amount, account holder has to sign on the back of NSC certificate and surrender the certificate to Post Master.

National Savings Certificate Interest Rate

NSC Interest Rate is 7.7% compounded annually but payable at maturity. National Savings Certificate interest amount is taxable. NSC Account Holder does not receive interest earned but it gets re-invested and compounded annually.

Who can open National Saving Certificate Account

- A single adult

- Joint Account (up to 3 adults)

- A guardian on behalf of minor or on behalf of person of unsound mind

- A minor above 10 years in his own name

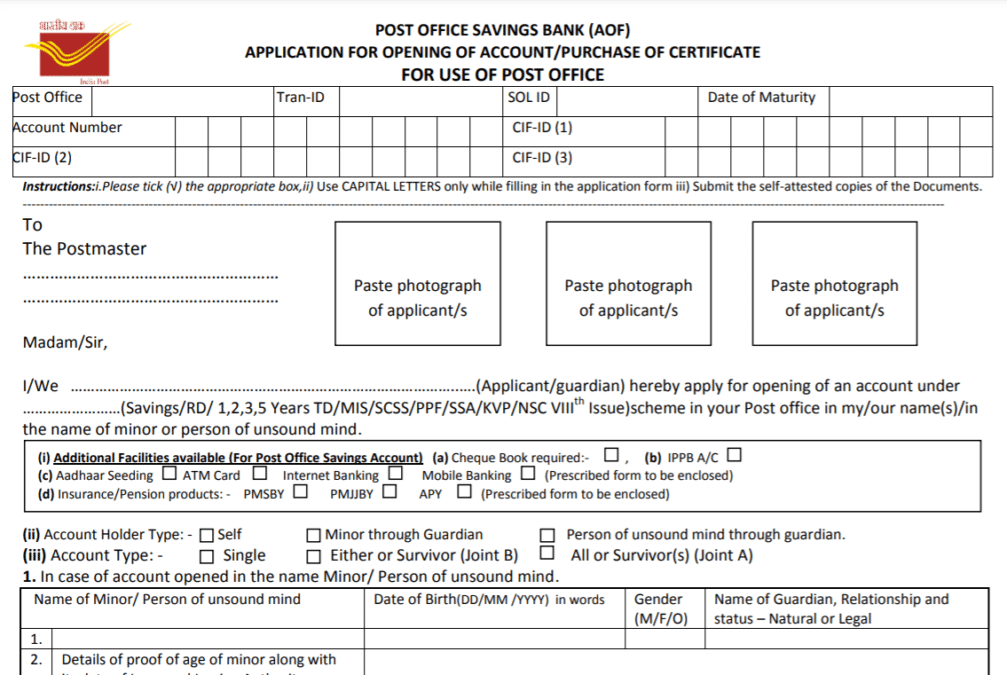

National Savings Certificates Account Opening Form

National Savings Certificate Account Opening Form is available at the official link at https://www.indiapost.gov.in/Financial/Pages/Content/Post-Office-Saving-Schemes.aspx

At this page, click at the National Savings Certificates link and in this section, click at the "Forms Available" link or directly click at the link here - https://www.indiapost.gov.in/VAS/Pages/Form.aspx#SavingCertificates

In the new opened page, click at the Download PDF link in front of "Application Form for Purchase of Certificate" to open the National Saving Certificate purchase online form as below:-

Fill up this NSC form and submit it at the nearest Post Office branch, get it approved and then you would be able to purchase certificate.

National Saving Certificates Calculator

Moreover, subscribers can calculate their interest amount in National Saving Certificate Scheme NSC using the link given below:-

https://groww.in/calculators/nsc-calculator/

Tax Benefits of National Savings Certificates

Subscribers should invest in National Savings Certificate Scheme due to the following reasons:-

- People can save income tax on income upto Rs. 1.5 lakh.

- NSC provides guaranteed Interest Rate of 7.7% per annum and can be checked using National Saving Certificate Calculator.

- National Saving Certificate Maturity Period is only 5 years.

- This savings scheme is easily available at all Post Offices.

- Furthermore, Interest is compounded annually and is reinvested by default.

Along with the rebate of income tax, interest earned is also added to the original investment and is also eligible for tax break. For eg. if anyone purchases NSC Certificate worth Rs. 1000, then individual will get tax break on initial investment in 1st year. Moreover, people will also get tax rebate on additional NSC purchases and on interest earned.

Who Can Invest - Maximum and Minimum Investment Amount

Any Individual who is looking for safe investment option, guaranteed interest and capital protection can invest in NSC. This investment option is easily available accessible than other tax saving methods. However, NSC is unable to beat inflation beating results as other investments like Tax Saving Mutual Funds and National Pension System. Minimum investment amount is Rs. 1000 and then in multiples of Rs. 100 while there is No Maximum Limit.

- Minimum Rs. 1000 and in multiple of Rs. 100, no maximum limit.

- Any number of accounts can be opened under the scheme.

- Deposits qualify for deduction under section 80C of Income Tax Act.

Any person who wants to open National Saving Certificate Account can do it through minimum investment of only Rs. 1000. Moreover, there is no maximum limit and can purchase any number of denominations of Rs. 100, Rs. 500, Rs. 1000, Rs. 5000 and Rs. 10,000. Afterwards, candidates will receive interest amount which can be checked using National Saving Certificate Calculator.

National Saving Certificate Payment - NSC Purchase

Buyer must submit Form A to purchase NSC account. For this, buyers can submit payment through Cash, Cheque, Pay Order, Demand Draft drawn in favor of Postmaster. Moreover, candidates can make payment from withdrawal funds of Post Office Savings Bank Account.

Accordingly, Postmaster will issue a new NSC Certificate on the spot or provide a provisional slip for purchase of certificate. These national savings scheme nss certificate can also get transferred from 1 post office to another.

NSC vs PPF vs KVP vs ELSS vs NPS vs FD

Here we are comparing NSC with other tax saving instruments like Equity Linked Savings Schemes (ELSS), National Pension System (NPS), Public Provident Fund (PPF) and Tax-saving Fixed Deposits (FD). This comparison is on the basis of National Saving Certificate Interest Rate, Lock In Period and Risk profile:-

NSC Comparison with other Schemes

| Investment | Rate of Interest | Lock in Period | Risk |

|---|---|---|---|

| National Saving Certificate (NSC) | 7.7% compounded p.a (Guaranteed) | 5 years | Risk Free |

| ELSS Funds | 12% to 15% (expected) | 3 years | Market Related Risks |

| Public Provident Fund (PPF) | 7.1% compounded p.a (Guaranteed) | 15 years | Risk Free |

| National Pension System (NPS) | 8% to 10% | Till Retirement | Market Related Risks |

| Kisan Vikas Patra (KVP) | 7.5% compounded p.a | 115 Months | Risk Free |

| Fixed Deposit | 6.9% to 7.5% (Guaranteed) | 5 years | Risk Free |

National Savings Certificate Issue & Maturity Period

The deposit shall mature on completion of five years from the date of the deposit. NSC has 2 types of issues - NSC VIII Issue and NSC IX Issue. Central govt. has discontinued NSC IX Issue in December 2015. Accordingly, only NSC VIII is open for subscription and comes with a lock in period of 5 years. There is no TDS on the interest earned so subscriber has to pay applicable tax on the total maturity value.

Loan on NSC Issue - People can also take loans from the banks against their investment in National Savings Certificates Scheme NSC. For this reason, subscriber has to transfer their certificate in the name of bank from which he / she is seeking loan. However, people cannot cannot make NSC withdrawal prematurely.

NSC Nomination Facility & Issuance of Duplicate Certificate

People can make nomination and select their nominee at the time of purchase through filling Form 1 or before NSC maturity in Form 2. This nominee can claim the maturity amount if the original account holder dies. This nominee can encash NSC at any time before or after NSC Maturity and can perform following operations:-

- Encash the National Savings Scheme NSS Certificate.

- Sub-division of NSC Certificate in suitable denominations in favor of individual nominees.

For this, nominee must intimate the Postmaster about the death of original account holder by submitting Death Certificate.

National Savings Certificate - Premature Encashment / Withdrawal

Premature withdrawal is not applicable in case of NSC. However, NSC can be encashed prematurely before 5 years under following conditions:-

- On the death of a single account, or any or all the account holders in a joint account.

- On forfeiture by a pledgee being a Gazetted officer.

- On the orders of court of law.

If National Savings Certificate Scheme (NSC) account is encashed within 1 year, then no interest is provided. In case the withdrawal is after 1 year then candidates will get interest but with discount.

Pledging of Account in National Saving Certificate

NSC may be pledged or transferred as security, by submitting prescribed application form at concerned Post Office supported with acceptance letter from the pledgee. Transfer/pledging can be made to the following authorities.

-> The President of India/Governor of the State.

-> RBI/Scheduled Bank/Co-operative Society/Co-operative Bank.

-> Corporation (public/private)/Govt. Company/Local Authority.

-> Housing finance company.

Transfer of Account from 1 Person to Other in National Savings Certificates Scheme

-> NSC may be transferred from one person to another person on the following conditions only:-

(i) On the death of account holder to nominee/legal heirs.

(ii) On the death of account holder to joint holder(s).

(ii) On order by the court.

(iii) On pledging of account to the specified authority.

National Savings Certificate VIII Issue Rules

National Savings Certificate VIII Issue Rules can be checked using the link - https://www.indiapost.gov.in/VAS/DOP_PDFFiles/Savings%20Bank/National%20Savings%20Certificates%20%28VIIIth%20Issue%29%20Scheme%20%202019%20English.pdf

National Saving Certificate - Highlights at a Glance

The important features and highlights of National Saving Certificate are as follows:-

| CScheme | Interest Rate | Minimum and Maximum Balance | Important Features |

|---|---|---|---|

| National Savings Certificate - NSC VIII Issue |

| Minimum Rs. 1000 and multiples of Rs. 100, No Maximum limit |

|

References

-- Furthermore for any query, candidates can visit the official website indiapost.gov.in