Subsidy on Home Loans for Families Not Covered in Pradhan Mantri Awas Yojana Gramin (PMAY-G): Ministry of Rural Department, Central govt. has launched Rural Housing Interest Subsidy Scheme (RHISS) 2026. Subsequently, this Rural Housing Interest Subsidy Scheme (RHISS) will provide necessary resources to the families which are not covered under PMAY-G. Accordingly, PMAY-G Home Loan Interest Subsidy Scheme will provide easy and cheap access for institutional loans at the subsidized interest rates for the construction or modification of their houses. In this article, you can know how to check eligibility, rate, tenure, discount, fillup claim form and complete details here.

Central Nodal Agency – Ies is responsible to implement this Interest Subsidy scheme. All the rural families whose name is not on the wait-list for PMAY-G can apply for this scheme. Central Nodal Agency (CNA) will approve Primary Lending Institutions (PLIs) to simplify the loan process. This scheme will provide coverage to all the Indians except the towns under Census 2011 and towns under PMAY (Urban).

RHISS will provide this loan to construct a new house or to modify a Kuccha house into a Pucca House. Moreover, these pucca houses should comply with the standards and can withstand normal wear and tear, natural disasters for at-least 30 years.

What is Rural Housing Interest Subsidy Scheme (RHISS)

To ensure housing for all by 2022, central government launched Pradhan Mantri Awas Yojana Gramin (PMAY-G) which came into effect from 1st April 2016. The PMAY Gramin scheme provides financial assistance to households living in rural areas who are houseless or living in zero, one or two room kutcha houses as per Socio Economic Caste Census (SECC) 2011 data and verified by Gram Sabha. PMAY G covers most vulnerable section of rural population deprived of housing and gives them housing assistance.

Since the objective of govt. is to provide housing for all by 2022, it is pertinent to ensure that adequate resources are made available to such households who are not covered under PMAY-G. In this direction, Ministry of Rural Development has come up with Rural Housing Interest Subsidy Scheme. RHISS would provide cheap and easy access to institutional loan to households living in rural areas and not covered under PMAY-G for construction / modification of their dwelling unit.

RHISS envisages providing loan to rural household at subsidized interest rate to enable them to construct / modify dwelling unit.

Scope of Rural Housing Interest Subsidy Scheme (RHISS)

PMAY Gramin for rural areas has been launched with an objective to provide pucca house with basic amenities to all houseless and households living in kutcha houses by 2022. To achieve the objective of Housing for All, around 2.95 crore houses would be constructed by the year 2022. PMAY-G covers those families of rural areas who are homeless or living in 0, 1 or 2 room kutcha houses as per SECC 2011 data.

But there are large number of rural families who lives in kutcha house with more than 2 rooms or pucca house with one or two rooms. These households also require support to construct a pucca house or modify / enlarge their dwelling units. To provide adequate resources to those families who are not covered under PMAY-G, a new RHISS has been launched. Rural Housing Interest Subsidy Scheme will provide easy access to institutional loan to all such needy households for construction / modification of their dwelling units.

The universe of beneficiaries, eligible to receive central assistance under RHISS scheme, will include any rural household which does not appear / figure on permanent waitlist for Pradhan Mantri Awas Yojana Gramin (PMAY-G). The RHISS has been effective and operationalised and aims to provide assistance to households in rural areas to construct houses or modify their existing dwelling units.

Beneficiaries / Coverage of Rural Housing Interest Subsidy Scheme (RHISS)

- Beneficiaries – All the rural households whose name does not appears in the permanent wait list of Pradhan Mantri Awas Yojana – Gramin are eligible to apply.

- Exclusion – RHISS will cover all the citizens of the country but will exclude those who belongs to the statutory towns of Census 2011 and towns which are covered under PMAY-Urban.

- RHISS will provide support for modification of existing dwelling units and construction of pucca houses as per eligibility criteria defined here with basic civic infrastructure like water, sanitation, electricity etc.

Definition of Pucca House under PMAY Gramin Home Loan Interest Subsidy Scheme

The pucca houses constructed / modified under RHISS should conform to norms and standards provided in extant guidelines on construction and structural safety in the country. A pucca house is one which is able to withstand normal wear and tear due to usage and natural forces including climatic conditions, with reasonable maintenance for at-least 30 years. The roof and wall of the house should be strong enough to be able to withstand the climatic conditions of the place in which the beneficiary resides and incorporate disaster resilient features, wherever needed, to be able to withstand earthquakes, cyclone, floods etc.

Primary Lending Institutions (PLIs) for RHISS Scheme

Central Nodal Agency (CNA), identified by the Ministry for purpose of implementation of Interest Subsidy Scheme for Rural Housing, would successfully implement this scheme. CNA will provide subsidy to the Primary Lending institutions (PLIs) and will also monitor the progress. Accordingly some of the PLIs are as follows:-

- Scheduled Commercial banks

- Housing Finance Companies

- Urban Co-operative banks

- State Co-operative banks

- Regional Rural banks (RRB)

- Small Finance banks

- NBFC-Micro Finance Institutions

- Other Institution identified by CNA

- Any other Institutions as identified by Central Nodal Agency and approved by Ministry of Rural Development

CNA will provide reports to the Ministry of Rural Development on monthly or quarterly. All the beneficiaries who are taking the benefits of other govt. schemes cannot apply under this scheme.

Interest Subsidy Features under Rural Housing Interest Subsidy Scheme

Beneficiaries seeking housing loans from Banks, Housing Finance Companies and other such notified institutions, for modification / construction of pucca houses in rural areas would be eligible for interest subsidy with following features:-

| Features | Rural Housing Interest Subsidy Scheme (RHISS) |

|---|---|

| Rate of Interest Subsidy | 3% |

| Maximum Housing Loan Tenure (Duration) | 20 years |

| Minimum eligible Loan Amount for Interest Subsidy | Rs. 2 lakh |

| Rate of Discount for Interest subsidy to calculate NPV | 9% |

The interest subsidy will be at the rate of 3% on principal amount of the loan for beneficiary. Subsidy shall be admissible for a maximum loan amount of first Rs. 2 lakh, irrespective of quantum of housing loan, for 20 years or full period of loan, whichever is less. If quantum of housing loan, however, is less than Rs. 2 lakh, the subsidy will be calculated on actual loan amount.

The Net Present Value (NPV) of Subsidy will be calculated based on notional discount rate of 9% for the period of loan and interest chargeable at the time the loan is contracted, upfront subsidy shall be released to Primary Lending Institution (PLI).

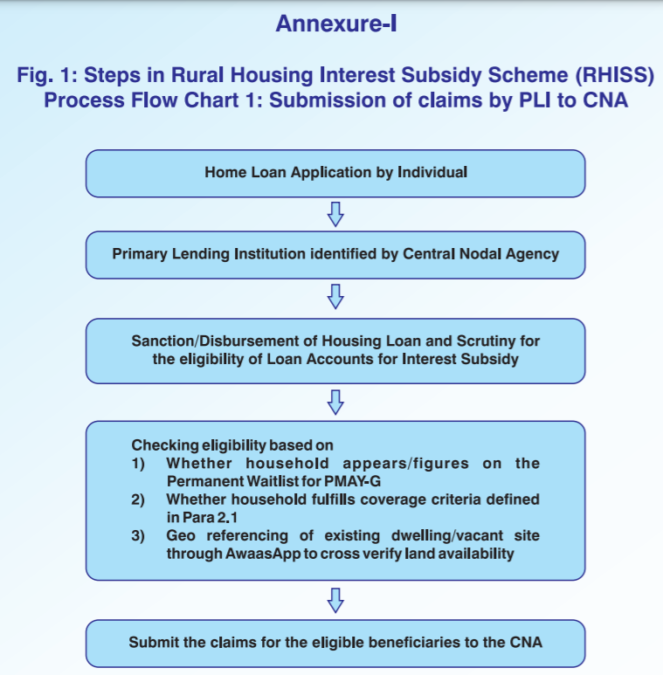

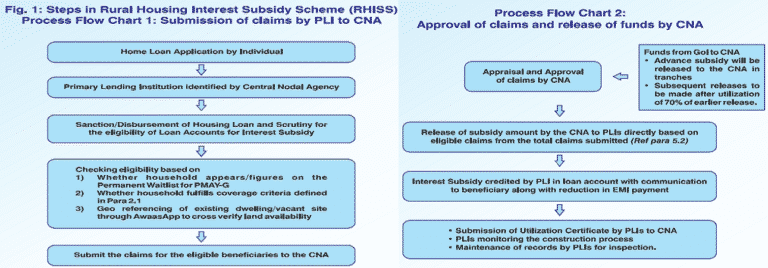

The NPV of interest subsidy given to PLI will be deducted from principal loan amount of the beneficiary, who will then have to pay interest to PLI at an agreed documented rate. fixed or floating on effectively reduced housing loan for the whole duration of the loan. The agreed documented rate which the beneficiary will have to pay may vary from bank to bank. The process flow diagram for the scheme is given here:-

Implementation Methodology of Rural Housing Interest Subsidy Scheme

- The interest subsidy will be available only for housing loan amounts indicated above and additional amount of housing loan beyond the above specified limit, if any, will be at non-subsidized rate.

- Net present value of the interest subsidy will be credited upfront to the housing loan account of beneficiaries through PLIs resulting in reduced effective housing loan and Equated Monthly Installment (EMI).

- National Housing Bank (NHB) has been identified as Central Nodal Agency (CNA) to channelize this subsidy to lending institutions and for monitoring the progress. Ministry may notify other institutions as CNA in future.

- Primary Lending Institutions (PLIs) identified as Scheduled Commercial Banks, Housing Finance Companies, Regional Rural Banks, NBFC MFIs, or any other institution may be identified by the Ministry, can register only with one CNA by signing MoU as per Annexure 2 of RHISS guidelines (download Guidelines through the link at the bottom of the article).

- CNA will be responsible for ensuring proper implementation and monitoring of the scheme and will put in place appropriate mechanisms for the purpose. CMA will provide periodic monitoring inputs of MoRD through regular quarterly and monthly reports or as required by the Ministry.

In case a borrower who has taken a housing loan and availed of interest subsidy under any other scheme of Govt. of India but later switches to another PLI for balance transfer, such beneficiary will not be eligible to claim the benefit of interest subsidy again.

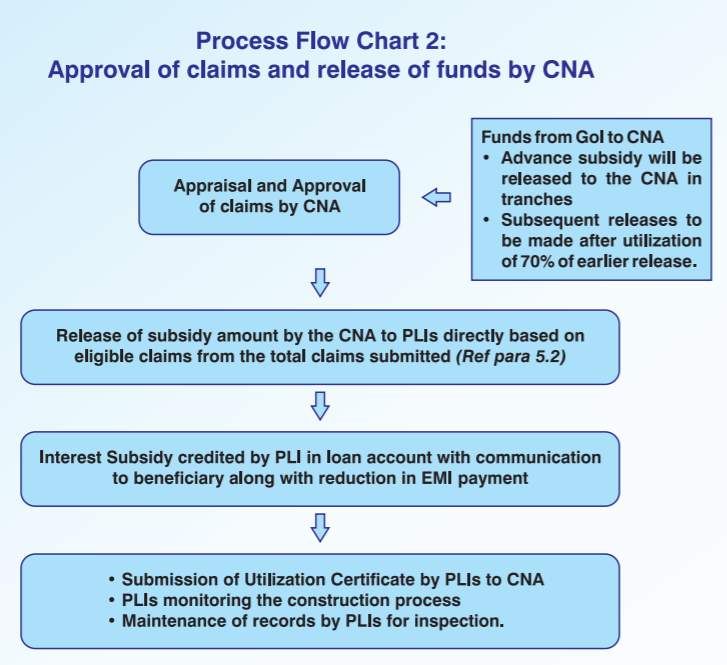

Mechanism for Release of Central Subsidy

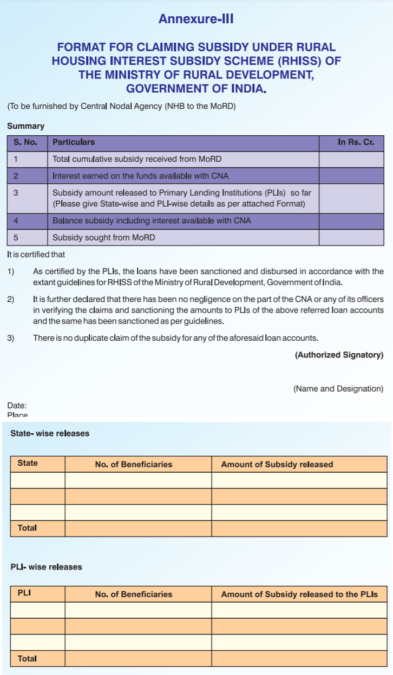

- An advance for Subsidy payment will be released to CNA(s) at the start of the scheme. Subsequent amounts of interest subsidy will be released to CNA(s) after 70% utilization of earlier amounts, on quarterly basis, and based on utilization / end use certificates submitted by PLIs to CNAs, as per prescribed format at Annexure 3.

- Based on the loan disbursed by a PLI to RHISS beneficiaries, the CNA will release the subsidy amount to PLIs directly based on claims submitted on total loans disbursed.

- NPV of interest subsidy will be credited by the PLI to the beneficiary’s account upfront by deducting it from principal loan amount of the beneficiary. The beneficiary will pay EMI as per lending rates on the remainder of principal loan amount.

- 0.25% of the total fund disbursement by the CNA to the PLIs will be paid to the CNA for their administrative expenses.

- In lieu of the processing fee for housing loan for the borrower under the scheme, PLI will be given a lump sum amount of Rs. 2000 per sanctioned application. PLIs will not take any processing charge from the beneficiary under the scheme.

Monitoring and Implementation of the Scheme

- RHISS will be implemented and monitored by the Ministry of Rural Development, Government of India through Central Nodal Agency.

- In addition to the state government, the State Level Bankers Committee (SLBC) will monitor the Scheme in the state through its prevalent institutional mechanism.

- In case any false declaration by the beneficiary under the scheme, she / he would be able for legal proceedings under relevant laws.

- All constructions / modification would be geo-referenced, time and date stamped and captured on AwaasSoft through AwaasApp.

- The decision of MoRD shall be final under the scheme.

Overview of PMAY-G Home Loan Interest Subsidy Scheme – RHISS

The highlights and details of PMAY-G Home Loan Interest Subsidy Scheme – RHISS are as follows:-

- Beneficiaries will get home loans for construction/ modification of the houses at an interest subsidy of 3 per cent.

- RHISS will provide a maximum loan amount of Rs 2,00,000 for a tenure of 20 years or full duration of the loan.

- However, if loan amount is less than Rs 2 lakh, then subsidy is calculated on the actual amount of the loan.

- Accordingly, Govt. will calculate Net Present Value (NPV) of subsidy at a discount rate of 9% for the duration of loan in addition to the interest charged at the time of loan.

- Subsequently, RHISS will release the subsidy to the Primary Lending Institution (PLIs).

- The process flow of this scheme is shown in the figure given below:-

References

For any further query, candidates can see the details of Rural Housing Interest Subsidy Scheme (RHISS) using the link given here – https://iay.nic.in/netiay/PMAY-G%20BOOK%20English.pdf